In Feb 2020, the MIT Sloan Management published 9 Megatrends That Will Shape the World in 2030 such as climate change, transparency, and nationalism that will be driving the workforce 10 years from now.

McKinsey shared their Understanding and shaping consumer behavior in the next normal as of July 2020 and it’s down to Behavioral Science which tells us that identifying consumers new beliefs, habits and “peak moments” is central to behavioural change.

Five actions can help companies influence consumer behavior for the longer term:

- Reinforce positive new beliefs

- Shape emerging habits with new offerings

- Sustain new habits, using contextual cues

- Align messages to consumer mindsets

- Analyze consumer beliefs & behaviours at a granular level

Very timely, the even brilliant HBR conducted the same research in 2013 and 2020 (during lockdowns) and the results are in late Aug 2020: Knowledge Workers Are More Productive from Home. This materialise as:

- more effective prioritisation of our work

- making time for work that matters most to us

- work is more important, less tiresome and contributes to the company’s objectives

The concerns are interesting:

- challenges of getting started on something new (the forming/storming stages of team development)

- and the note on training & development interestingly reflects the perceived bias regarding “e-learning”: While time spent on self-education went up during lockdown, this was mostly due to online webinar and course attendance— which helps build knowledge but doesn’t encourage the active experimentation and personal reflection that help us really grow.

Unfortunately, online learning has a bad reputation as people imagine lonely hours staring at a screen, listening ot a lecturer. This is the opposite of Hyper Island’s learning by doing approach and during the pivot this year due to Covid, all face-to-face learning journeys were not ‘translated from offline to online’ but completely reimagined as gamified and immersive learning journeys, complete with murder mysteries and virtual tours of Silicon Valley.

Back to HBR, heres’s the 2013-2020 comparison:

- Lockdown has helped us more effectively prioritize our work.

- We have been taking more direct charge of our time during lockdown. We don’t have colleagues or bosses badgering us, and we don’t get drawn into meetings by force of habit, just because we happen to be around. The result is a reassuring increase in us making time for work that matters most to us.

- In 2020, respondents say their work is more important, less tiresome, less easily offloaded and contributes to the company’s objectives. Not only is their work important, they feel important as well! Of course, there is some self-justification going on here: When we think our work is important, we are more likely to gain personal utility from it and less prone to delegate it. But it seems there is also some reprioritization occurring, with people stopping some of the less-important activities they used to do and focusing their energy in a more effective way. Overall, the findings here are consistent with the notion that knowledge workers are more intrinsically motivated — and taking more personal ownership — during lockdown, in large part because of the increased degrees of freedom they are getting.

Forbes’ The Science Of Virtual Work—and How It Can Make Life Easier For Everyone argues for working from home early in the pandemic (during March 2020 lockdows) citing a 2015 Stanford study of 500 employees over two years showed that working remotely increased total-factor productivity by between 20-30%, due in part to increased performance and lower overhead costs. They summarise the early reluctances as: expedience bias, safety bias, distance bias (where we unintentionally exclude people ie. “If you’re not actively including, you’re probably accidentally excluding.”).

And Business News Daily highlighted the toll on workers as 29% of remote employees said they struggle with work-life balance, and 31% said they have needed to take a day off for their mental health (offering breaks and the pomodoro technique as a solution). It was interesting to read about the balance between performance / productivity and relationship: Office workers spent an average of 66 minutes per day discussing nonwork topics, while remote employees only spent 29 minutes doing the same. And see that managers were found to be particularly distracting, as they were found to spend nearly 70 minutes talking about nonwork topics compared to the 38 minutes spent on average by nonmanagers.

The ultimate analysis on the future of remote work came from McKinsey end of 2020 with An analysis of 2,000 tasks, 800 jobs, and nine countries, showing that the potential for remote work is determined by tasks and activities, not occupations. As a consequence,

In the US workforce, we find that just 22 percent of employees can work remotely between three and five days a week without affecting productivity. In contrast, 61 percent of the workforce in the United States can work no more than a few hours a week remotely or not at all. The remaining 17 percent of the workforce could work remotely partially, between one and three days per week.

McKinsey analysed the Chinese consumers changing shopping habits post COVID19 in May 2020 and it is packed with data for over 100 million shopppers. The case for change is clear:

- Continue to protect customers and employees

- Drive triple digital transformation: Manage your business in real time and digitally; Don’t just sell online, engage your customers digitally end-to-end; Transform your business model

- Align with consumer trends: healthy, local, and delivering value

- Transform your supply chain to be agile and resilient

Tech can improve efficiency by 2-5 percent of sales and, depending on starting position, drive sales and make or break market share during a crisis. Retailers need to pursue a triple transformation of people (new capabilities and ways of working), technology (modularizing core tech and deploying software-as-a-service across the value chain) and business (delivering value for the customer).

Think with Google – The retail road to recovery: Tips on how retailers can better connect to consumers shows the June 2020 GlobalWebIndex: 38% of APAC consumers who weren’t online shoppers prior to the pandemic say they intend to continue to shop online.

“A Peek into your Consumer’s Future 2020” report from Think with Google highlights 3 consumer shifts: With Me, All to Gather, Shared Commerce and it shows the influence on marketing of brands and businesses within APAC. The report is packed with intell & nice references to APAC startups.

Interesting trend exacerbated by lockdowns hightlighted in Get Wired podcast: The rise of virtual beings. Think influencers, sex workers, gurus or public speakers, VC not needing breaks, travel, food which is very appealing during quarantines & lockdowns. This ties to HBR’s The Era of Antisocial Social Media: Digital campfires like private messaging, micro-communities, and shared experiences with examples of NFL, Marvel, Nike in Fortnite to reach audiences; they sell skins (weapons/outfits for in-game avatars), create branded mash-up game modes, drop limited-edition product inside the game.

While the Freakonomic radio answers an age-old question: Does Advertising Actually Work? And the short answer is: doubling the amount of [TV] advertising would lead to about a 1 percent increase in sales.

The McKinsey podcast from 4 Aug 2020 Meet Generation Z: Shaping the future of shopping shared that Gen Z archetypes are similar to other categories of customers, they break down into the same 7 segments as the rest of the total population across 3 clusters and it is not about life stage:

- Value customers

- Quality customers

- Image cluster -> this is a movement across ages (moving from value)

Couple this with Decoding the ‘messy middle’ of purchase journey from Think with Google which is based on Behavioral Sciences and highlights our 2 mental modes (between the triggers and purchase) and 6 cognitive bias that influence purchase decisions (Category heuristic, Power of now, Social proof, Scarcity bias, Authority bias, Power of free)

Google “messy middle” follow-on: how behavioural science can be used to increase the effectiveness of Search ads:

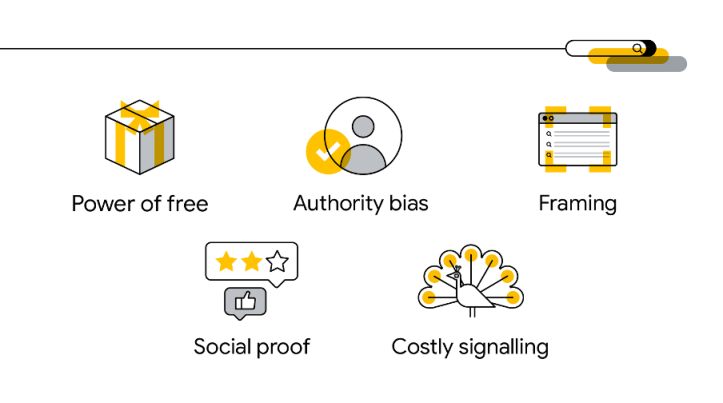

We used the following five behavioural science principles to alter the ad copy, in an attempt to move consumer interest away from the favourite brand:

- Power of free: Free items, offers, and vouchers with a purchase can be a big motivator.

- Authority bias: When brands, products, and services are backed by experts and trusted sources, they stand out from the competition.

- Social proof: Reviews, recommendations, and highlighting a popular choice within a relevant reference group can be very persuasive.

- Framing: Changing the frame of reference can help people reconsider the value of a product or service. For example, framing can highlight benefits such as convenience or time-savings.

- Costly signalling: Demonstrating the premium nature of a product through premium associations, such as an ad during the Super Bowl.

One at a time, we altered the ad copy of the brands to test the effectiveness of the different principles (also known as biases). By doing so, we were able to shift preference away from the shopper’s favourite brand. Even though, in some instances, the shopper had never even heard of the brand as it was a fictional one.

Takeaway: When used intelligently and responsibly, behavioural science principles are powerful tools to win and defend consumer preference in the “messy middle”.

Automation can help you be creative with your ad copy while systematically testing which changes make the biggest impact for your brand and product. Takeaway: Even if you’re not top of the Search results page — or no one has heard of your brand — you can close the gap between trigger and purchase by supercharging your ad copy.

Also from Think with Google, with consumer behaviours changing, 3 ways first party data can help you stay on top: it shows the value of a connected data-driven strategy with nice examples around the world. And the power of first-data with BCG study confirms that companies linking all 1st party data sources outperform those with limited data integration:

- incremental revenue from single ad placement, communication, or outreach up to x2

- perform x1.5 better in cost efficiency metrics

And Why conversion modeling will be crucial in a world without cookies:

Conversion modeling refers to the use of machine learning to quantify the impact of marketing efforts when a subset of conversions can’t be observed. For example, when measuring conversions across devices, there may not be cookies available to link these devices. In this case, you’ll be unable to attribute some of your conversions to the corresponding customers who interacted with an ad. If no modeling techniques are employed, this attribution problem will leave holes in the customer journey, prohibiting you from fully understanding your customers’ paths to conversion. But with a modeling foundation in place, observable data can feed algorithms that also make use of historical trends to confidently validate and inform measurement. Modeling enables accurate measurement while only reporting on aggregated and anonymized data. This unlocks a full, privacy-centric picture of your customer behavior, ensuring that your performance doesn’t suffer just because direct measurement isn’t always possible.